Non-Resident Indians (NRIs) often face significant foreign exchange (forex) risks when managing their earnings, investments, and remittances across different currencies. Currency fluctuations can impact the value of their income, savings, and assets, leading to financial uncertainty. Whether it’s sending money home, investing in Indian markets, or repatriating funds, exchange rate volatility can erode returns and affect long-term financial planning.

Check – Best NRI investment options in India

Understanding the impact of forex risk and implementing effective strategies—such as hedging, diversification, and timing remittances wisely—can help NRIs safeguard their wealth and optimize their financial decisions in an unpredictable currency market.

Credit: This post is written by Vidya – she is NRI (Data Dec 24)

Impact of foreign exchange risk for NRIs

S&P Global Ratings has forecasted India’s GDP growth to be 6.7% for 2025-26 and 6.8% for 2026-27. With a growing economy and a variety of investment options, India is an appealing destination for NRIs seeking to expand their financial portfolio. However, the exchange rate (the rate at which one currency can be exchanged for another) plays a critical role in the financial outcomes for NRIs, who can be investors, consumers, and business owners with interests in India.

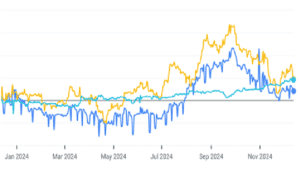

Check the change in value over the last year in these currency pairs:

Fluctuations in exchange rates of Indian rupee versus the US dollar, British pound and Singapore dollar

Typically NRIs deal in two main currencies – the Indian rupee and the currency of their country of residence. Many NRIs (who do not live in the USA) also deal in US dollars. They have to deal with exchange rate fluctuations between these currencies:

· As a consumer travelling from abroad to India, a favourable exchange rate (stronger resident country currency or US dollars) can increase purchasing power and make travel and shopping in India more affordable.

· As an investor in India, appreciation of the Indian rupee can increase the value of their investments in India.

· Conversely, currency depreciation or volatility can pose risks to investments done through repatriations to India. For instance, if an NRI has used his income in US dollars to convert to INR and invested in India and the INR depreciates against the USD, he will get less money when he transfers the money back to the US. Similarly, returns on these investments will be lower than projected when the Indian Rupee depreciates against the US dollar.

- If an NRI services interest payments for a loan taken in India, depreciation in the Indian rupee will lead to less outflow of the foreign currency, and appreciation will lead to more outflow.

Financial goals are also affected by currency fluctuations. For instance, consider a US-based NRI’s goal of funding their child’s college education in about ten years. The NRI invests US$ 50,000 at 7% per annum in an NRE fixed deposit to achieve this. Converting this to Indian rupees, this would be around ₹42,40,000. In ten years, this would grow to approximately ₹83,40,700. If the child studies in India, there will be no exchange rate impact as the amount is in INR already and in an Indian bank account. However, if the child decides to pursue studies in the USA, the exchange rate will play a role in determining the value of the investment. If the exchange rate is ₹75 for US$1, the amount received after conversion will be US$ 111,200, and at ₹85 to a dollar, the amount received will drop to US$ 98,100. (For simplicity, the average interest rate is taken, and taxation is not considered).

As you can see, the exchange rate affects the value of investment. Therefore, NRIs need to factor in exchange rate fluctuations when planning their financial strategies. Here are some ways to manage exchange rate fluctuations:

Classify financial goals based on currency Requirements

When setting financial goals, classify them based on the currency in which the funds will ultimately be needed. For example, if you’re planning a holiday abroad, you can set the goal in USD, while an investment in real estate in India should be tied to INR.

Invest in India through offshore funds

You can invest in the Indian market through offshore funds. Offshore funds are equity funds that invest in Indian companies, and you can invest and redeem using your foreign currency. Do consider aspects like minimum ticket size of investment, taxation, charges, jurisdictional and country restrictions and the underlying portfolio to ensure that the fund is aligned to your financial goals and asset allocation plan.

Diversification

Portfolio diversification is key to managing financial risk. For NRIs, diversifying investments can help mitigate the risks associated with currency fluctuations and repatriating funds. This involves spreading investments across:

- Asset classes: Investing in different assets like stocks, bonds, real estate, and other assets can help balance the risk-return ratio in the portfolio.

- Geographic regions: Spreading investments across different countries or regions can reduce the impact of regional economic downturns and volatility.

Check – Financial Planning for NRIs

Hedging

Currency derivative trading is an exchange of two currencies at an agreed price at a future date. The exchange of currency can be done by dealing in currency futures or currency options. NRIs can take positions in currency derivatives to hedge the currency risk. It can be done to the extent of the market value of their rupee investments in debt and equity, dividends due to them, and the balances held in NRE bank accounts. They can work with an Authorised Dealer bank (Category 1 bank) that is a clearing member of the exchange or the clearing corporation. Currently, this is possible for four currency pairs –

- USD-INR

- EUR-INR

- GBP-INR and

- JPY-INR

While currency derivatives can help manage currency exchange risk, they are complex products and involve high risk, especially for retail investors. Volatility in the market, country risk in terms of stability, and transaction risk in terms of the time differential between entering and settling a contract are some risks in currency derivatives that can lead to significant losses.

Professional guidance

You can consult with a financial expert who has the requisite skill and experience in providing personalized support to NRIs in managing exchange rate risks. They will be able to design an investment strategy that is tailored to your unique financial position and provide continuous support per evolving NRI-specific investment regulations and global market conditions.

As an NRI, you have access to global markets and investment opportunities. By creating a financial strategy that helps you navigate currency volatility, you can optimise your investments and secure your financial future.

Managing foreign exchange risk is crucial for NRIs to protect their wealth and maximize returns. By adopting smart strategies like hedging, diversification, and timing transactions wisely, they can navigate currency volatility effectively.

Have you faced forex challenges? Share your experiences or ask questions in the comments—we’d love to hear from you!